Earn Now, Pay Later: The Curious Case of Switching from Income to Consumption Tax

- v2v4youth

- Apr 11, 2025

- 6 min read

1 Introduction

Amid the hype surrounding Elon Musk’s Department of Government Efficiency (DOGE), much of the public attention has been directed toward streamlining government spending, be it improving operational workflow or cutting out entire government agencies. While these efforts are important, they address only one side of the equation. What if the issue is not only how the government spends its income, but also how and when it collects tax?

2 Changing Landscape

One of the most popular alternatives to the income-tax heavy model utilized by the United States is consumption taxes. Since the 1990s, most OECD countries have reduced income tax and increased consumption tax, most often as a federal value-added tax (OECD). However, some countries like the United States share a complicated colonial history with consumption taxes. Even after a quarter of a millennium, the United States derives only a modest 15.7% of tax revenue from consumption taxes, compared to the OECD country average of 31.6% (Weigel & Bunn, 2024).

Fig 1: OECD Tax Revenue Sources.

Under the classical market for labor, income tax reduces labor supply, individual savings, and reinvestment (Gale & Samwick, 2014). Additionally, many upper socioeconomic echelons have the means to avoid income taxation by storing value in other assets. Consumption tax appears an attractive tax revenue alternative, since it encourages saving and investment, and is unavoidable when consuming legally (Marples, 2023). Specific consumption-oriented taxes already exist in the domestic economy, such as alcohol and cigarette taxes (Tax Rates, n.d.). In the global context of climate change and resource scarcity, consumption tax can address the wasteful consumerism and high per capita ecological footprint many first-world countries generate like the United States (Urry et al., 2017).

3 Economic Implications Model

3.1 Simple Model: Alice Spends Every Dollar She Earns

Let us first model the transition from income tax to consumption tax through a worker, Alice. She makes $60,000 a year. Currently, her country collects a 20% flat income tax (60,000*20%). This is monetarily equivalent to levying a 25% consumption tax (48,000 * 25%). This simple model demonstrates that the government is still able to collect the same amount of tax revenue in the end, just under a different name (see Table 2).

Table 2: Summary of the income tax and the consumption tax scenarios for Alice.

3.2 Two Account Model: Living Account and Savings Account

The first model makes it seem that both workers and the government are indifferent between income tax and consumption tax. Realistically, many people do not spend every earned dollar, instead saving and investing a portion of their income for retirement. Inflation also impacts wages and consumption prices.

Table 3: Breakdown of the two account system.

In this second model, Alice has two accounts: living account and savings account.

● Work and Retirement: Alice starts working at 23 years old, retires at 62 (MassMutual & PSB Insights, 2024), and has a life expectancy of 82 (Dvyik, 2024). Salary starts at $60,000 (US Bureau of Labor Statistics, 2024), increases 3% yearly (Hayes, 2023).

● Inflation: 3% annually (US Bureau of Labor Statistics, 2024).

● Consumption: 65% of salary pre-retirement; post-retirement, consumption drops to 80% of prior consumption levels at 62 years old, adjusted for inflation.

● Investment: Pre-retirement investment returns are projected at 7%, reflecting riskier investments like the stock market (Maverick, 2024); post-retirement investment returns are projected at 4%, based on bond returns (Reed, 2023).

3.3 Income Tax Scenario

Income tax affects both base income and earnings from investments.

Fig. 2: Account activities over Alice’s lifetime under the income tax scenario. The dotted black line represents her savings account balance, reaching its highest at 62, the retirement age (dotted orange line). At 82, Alice has no money in her savings account.

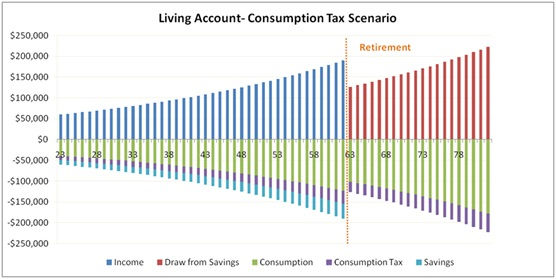

3.4 Consumption Tax Scenario

Investment returns are no longer taxed. Under the consumption tax scenario, the savings account retains a substantial balance of approximately $2.3 million by age 82, compared to zero in the income tax scenario. This money provides the retiree with additional flexibility.

Fig. 3. Account activities over Alice’s lifetime under the consumption tax scenario. The dotted black line represents her savings account balance, reaching its highest at 62, the retirement age (dotted orange line).

3.5 Comparison

Under both the income tax and the consumption tax scenarios, lifelong income, consumption, and tax payments remain the same monetarily. The only difference lies in the investment returns. Under the income tax system, lifelong investment income amounts to $2.6 million, compared to $4.9 million under the consumption tax scenario (Fig. 4). The key factor driving this difference is that savings and reinvestment are not taxed in the consumption tax scenario.

Fig. 4: Summary of quantitative differences between the two scenarios.

4 Macro Impacts of Consumption Tax

4.1 Short Term

Economic: Anticipating the substantial price increase, demand will spike for durable and expensive items (ex. laundry machines, cars) shortly before the implementation of the consumption tax (Nippon.com, 2020). Post-implementation, the sudden increase in prices will reduce consumption, particularly for high price-elasticity products and services. Overall tax revenue, now primarily reliant on the consumption tax, will go down, which may lead to a budget deficit. Additionally, the decrease in domestic consumption may trigger a recession (Australian Government, 2003). Certain consumption-heavy industries, such as tourism, may face precipitous decline as foreign visitors cannot afford as much.

The increased savings and capital inflow will increase stock market investments, accelerating speculative bubbles. Capital inflows increase demand for the country’s currency, leading to appreciation against other global currencies. A strengthened currency makes imported goods and services comparably cheaper, which may reduce impact domestic spending and country exports. In response to inflation, the federal government may implement monetary and/or fiscal policies to stabilize the market—thereby slowing overall economic growth.

Social: Current retirees and older workers approaching retirement are subjected to double taxation—once from their prior savings and income taxed under the legacy tax system, and again from the new consumption tax. The increase in cost of living presents an unanticipated burden, sparking an exodus of retirees who emigrate to countries with lower cost-of-living. Retirees would therefore oppose the shift to consumption tax.

4.2 Long Term

Economic: A consumption tax system encourages saving and reinvestment, driving long-term economic growth. Externally, the country becomes a tax haven, attracting foreign investments and high net-worth individuals. These individuals contribute both capital and talent, boosting the nation’s GDP and overall economic productivity.

Social: Higher-income and high net-worth individuals disproportionately benefit from increased savings and investment returns (Fig. 6), exacerbating social inequality. Higher-income individuals will enjoy disproportionately larger returns, and would therefore be in support of the change. However, lower-income individuals oppose consumption tax; a gradual transition from an income tax system to a consumption tax system could offer some reprieve.

Fig. 6: Simulation of savings balance at 82 years with varying annual incomes. Consumption accounts for a smaller percentage of total income in higher-income groups.

As a result of capital influx both domestically and internationally, especially from high-income individuals, as well as the inelastic supply of real estate, housing prices will spike (Chen et al., 2020). Vulnerable communities face significantly higher risk of gentrification, and lower-income persons would be disproportionately affected by the higher prices (Marples, 2023). Ironically, the consumption tax would thus reduce lower income persons’ ability to save and invest capital, a vicious cycle of poverty.

4.3 Effects on Foreign Relations

Capital Flow: Zero income tax will attract global capital inflows to this country, as capital seeks higher returns by minimizing tax burdens. The outflow of capital from foreign nations will reduce their economic growth.

Currency Appreciation: A significant inflow of capital will increase demand for the local currency, causing its appreciation. This strengthens imports but discourages exports.

Talent Flow: High-skilled workers will migrate from foreign countries to capitalize on the consumption tax policy, while retirees will move to countries with lower living costs. This dynamic may result in a "brain drain" for foreign nations, leading to slowed economic growth and reduced tax revenues.

4.4 Remediating Shortcomings of Consumption Tax

The consumption tax is regressive, disproportionately favoring richer groups. To acquire support for transitioning in democratic countries, consumption tax must also be qualified with redistribution.

● Low/Zero tax on essentials ensure these basics are affordable for low/fixed-income individuals, whose consumption accounts for a larger percentage of income (Sales Taxes and Their Impact on Low-Income Households, 2024).

● Higher tax rates for luxury goods (ex. private jets, prime real estate) ensure the wealthy contribute more money proportionally to the tax system for redistribution.

● Subsidize negatively impacted sectors (ex. hospitality, tourism) and groups (ex. Retirees, low-income people). Tax credits, rebates, or direct cash transfers would provide a financial buffer during the tax transition.

5 Conclusions

Contrary to classical American impressions like the Tea Act, consumption tax can encourage higher saving rates, increase investments, and boost economic growth, while enabling the same revenue for the government. Both domestic and foreign investors would favor replacing the income tax. However, consumption taxes inherently favor more well-off socioeconomic echelons and heat up volatile markets. A meticulous transition plan with careful execution is essential in minimizing short-term economic downturn and long-term socioeconomic inequality. It remains to be seen if consumption taxes can gain the same hype as DOGE.

Comments